A dilemma for clients and Brokers alike.

Short version;

- Engage your Mortgage Broker for a better understanding of this product.

- HomeEquity Bank Guarantees that the amount to be repaid will never exceed the fair market value of your home at the time that it is sold.

- No income requirement or credit or medical check

- Money is tax free

- No payments until home is sold

- Money can be a lump sum or monthly income with lump sums available

- Homeowner keeps any increase in the home’s value, but is never required to make up for a decrease in value

Clearly this is a topical issue, as I was finishing this post a similar story from today’s Globe & Mail hit my inbox.

Longer version;

In my last post I wrote about the difficulty many seniors now encounter when attempting to borrow against the equity in their home. Despite residing within an asset worth anywhere from hundreds of thousands to several million dollars, seniors have been caught up in Federal Lending guideline changes which are focused on pushing the underground economy above ground. Documented income from employment sources are now Vital, as the mainstream lenders have all had to collapse their Equity lending programs.

The catch is that these same programs were used regularly by retired folks to access the equity in their homes in order to extend their years in said home.

Lenders are not so much unwilling as they are simply not allowed to qualify a client using basement suite income, income from registered retirement savings, CPP and/or OAS.

This leaves many seniors, in particular those lacking a government pension or a strong corporate pension, looking to alternative lenders or, on occasion, private lenders for financing. Such financing comes at rather punishing interest rates as compared to where initial expectations are set. Private lenders, in particular, range from 5.75% – 12% on interest-only loans, where the principal is rarely paid down. Ostensibly the payments are set up as interest only to make them more affordable. However this sort of lending is something to be engaged in only where there is a clear exit strategy within six months to one year, and the funds are being used to facilitate said exit, i.e., to repair or slightly update a home in preparation for listing it for sale.

An exit strategy from a Private mortgage is crucial.

An exit strategy from a reverse mortgage has far greater flexibility around it.

For those with longer-term plans, reverse mortgages can be an option worth reviewing. On the interest rate ladder, a reverse mortgage is now only one step past conventional financing: as low as Prime +1.25% — significantly less expensive than private lending and on a par with some of the ‘Alternate’ or ‘B’ lenders in the market.

Yet Mortgage Brokers and financial planners are often reluctant to discuss this option, for a number of reasons.

Reason 1: More expensive

The first reason is that a conventional loan works out to be less expensive. If a senior does qualify for, say, a 5-year fixed mortgage for 50% of the home’s value at 2.99%, amortized over 30 years, the payments could in fact be quite manageable via investment revenue, suite income, or pension income. And ultimately, this will cost less than the reverse mortgage, as the table below shows. Reverse mortgages have reduced their interest rates of late, but they are still higher than those of conventional mortgages.

| 50% LTV Mortgage on $1 Million Home for 5 Years | ||

| Conventional Mortgage | HomeEquity Bank Reverse Mortgage | |

| Loan | $500,000 | $500,000 |

| Interest | 2.50% 5-year Variable, 30-year Amortization | 4.25% 5-year Variable |

| Monthly payment | $1,972.25 per month | $ZERO |

| Total 5yr interest | $58,601.63 | $115,673.30 |

| Balance | $440,266.63 (original loan minus principal paid down) | $615,673.30 (original loan plus accumulating interest) |

| 5yr Investment return potential | $500,000 invested @ 5% growth $138,140.78 | $500,000 invested @ 5% growth $138,140.78 |

| Home value growth | $159,274.07 @ 3% per year | $159,274.07 @ 3% per year |

| Total Net worth Change | $238,813.22 increase | $181,741.55 increase |

For anyone who can qualify, the conventional mortgage is nearly always the right choice.

As the above table shows, the conventional mortgage approval results in ~$57,000.00 greater net worth. However this was achieved at the expense of being able to carry a $1972.25 monthly payment.

The reverse mortgage option is more about eliminating payments, or creating an income supplement. It also works well for clients unable to qualify due to credit or income challenges.

Reason 2: Misconceptions

As a Broker, my own personal reluctance surrounding the reverse mortgage option does not stem from concerns about the product, nor from discussing it directly with the clients themselves. Rather, it is the fallout that flows from the people surrounding the clients, friends and family with outdated or inaccurate perceptions of the product.

Most of the negative connotations stem from misconceptions about rates based on outdated data, as well as a mixture of half-accurate data on products in the USA, which are notably different from our more Socialist style.

The majority of people, of all ages, lack an understanding the many positives within the product: no payments as long as the homeowner lives and occupies the property, no loss of the remaining equity in the property, lower rates than in previous years.

When the clients try (imperfectly due to the complexity) to explain their reverse mortgage they are often subjected to a litany of criticism: ‘They’re trying to take over your house‘, or ‘If house prices drop you could owe more than the house is worth‘, or ‘Anyone who would recommend one of those is a real shyster‘, or the classic, ‘But what about my inheritance?‘.

To address these in order:

- The client continues to own the house. The reverse mortgage provides financing against the asset. When the asset is sold the debt will be paid.

- The most that can be borrowed is 50% of the value. The lender will never foreclose if taxes and insurance are paid and the property is kept up. Over 99% of reverse mortgagors end up with some level of remaining equity.

- A Broker (at least THIS Broker) is only going to recommend a reverse mortgage after looking at ALL aspects of the client’s financial situation… financial circumstances that friends and family probably know nothing about. The reality is that few people in their 70’s with $100,000 of consumer debt wish to chat about it with anybody at all. Understandably.

- The reverse mortgage allows clients to invest money, repair and upgrade the home, enjoy predictable cash flow instead of selling off assets, live at home longer… activities that in all likelihood will increase or maintain the inheritance. (Besides, it’s their money to do with as they wish.)

Sadly the unfounded objections of the uninformed will likely cause guilt and fear in clients who often are already feeling like they’ve somehow failed in life because they want (or need) to borrow against their home in retirement. Brokers know that they will have to soothe, reassure, explain at length, and otherwise deal with the emotion that these third parties stir up. And often it is a no-win situation for the Broker involved.

Few Brokers I know would value a commission more highly than happy clients. After all, happy clients lead to the next set of (happy) clients.

Reason 3: Outdated view

As well as misunderstanding the product itself, many people are unaware of recent improvements that make a reverse mortgage a better option for more people.

CHIP (Canadian Home Income Plan) recently released updates to its reverse mortgage products.

- Interest rates lower (Variable at Prime +1.25% and fixed at 5.49%)

- Homes with existing mortgages are now eligible

- Eligible amount raised from 40% to 50% of assessed value

There are many other continuing advantages as well.

- No income requirement or credit or medical check

- Money is tax free

- No payments until home is sold

- Money can be a lump sum or monthly income with lump sums available

- Homeowner keeps any increase in the home’s value, but is never required to make up for a decrease in value

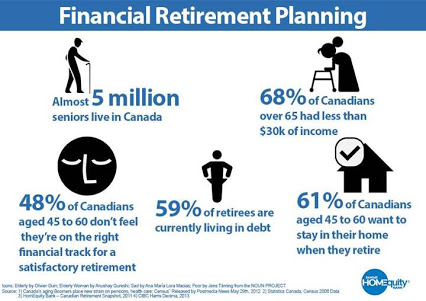

Considering the number of Canadians entering retirement while still carrying debt, the reverse mortgage deserves a second look. It can be a game-changer.