[vc_row][vc_column width=”1/1″]In the Vancouver market, we often hear about the benchmark price, the average price, and the median home price. Usually that of a specific neighbourhood or municipality.

However, what buyers rarely hear is the average price of the bottom 80% of listings of the Greater Vancouver Area. Y’know, the properties that the overwhelming majority of us live in.

A review of this significant market slice is overlooked because it is boring. Boring, because when we skim the ultra high end sales off the top, and look at the lower 80% of properties listed in the Lower Mainland we arrive at an average sale price of ~$597,000. Such a property ($597,000) would today require household income of ~$108,000 using a 5.8% down payment ($34,700) to qualify for purchase.

A $108,000 household income is certainly above the recently sighted average of $80,000, but not at all uncommon in the lower mainland in the era of the dual income household in which we currently live.

It is also worth noting that previous to Oct 17, 21016 the income required for this same purchase price was ~$88,000.00 per year. In other words an experienced police officer, teacher, nurse, or firefighter could pretty much pull that $597,000.00 purchase off on their own income.

The Federal Government

So, while ~80% of properties on the market were arguably within reach of the average household in the Lower Mainland prior to Oct 17, 2016 the federal government decided, in their infinite wisdom, that a household with an:

- excellent credit score

- Stable documented income

- zero consumer debt

- a $34,700.00 down payment

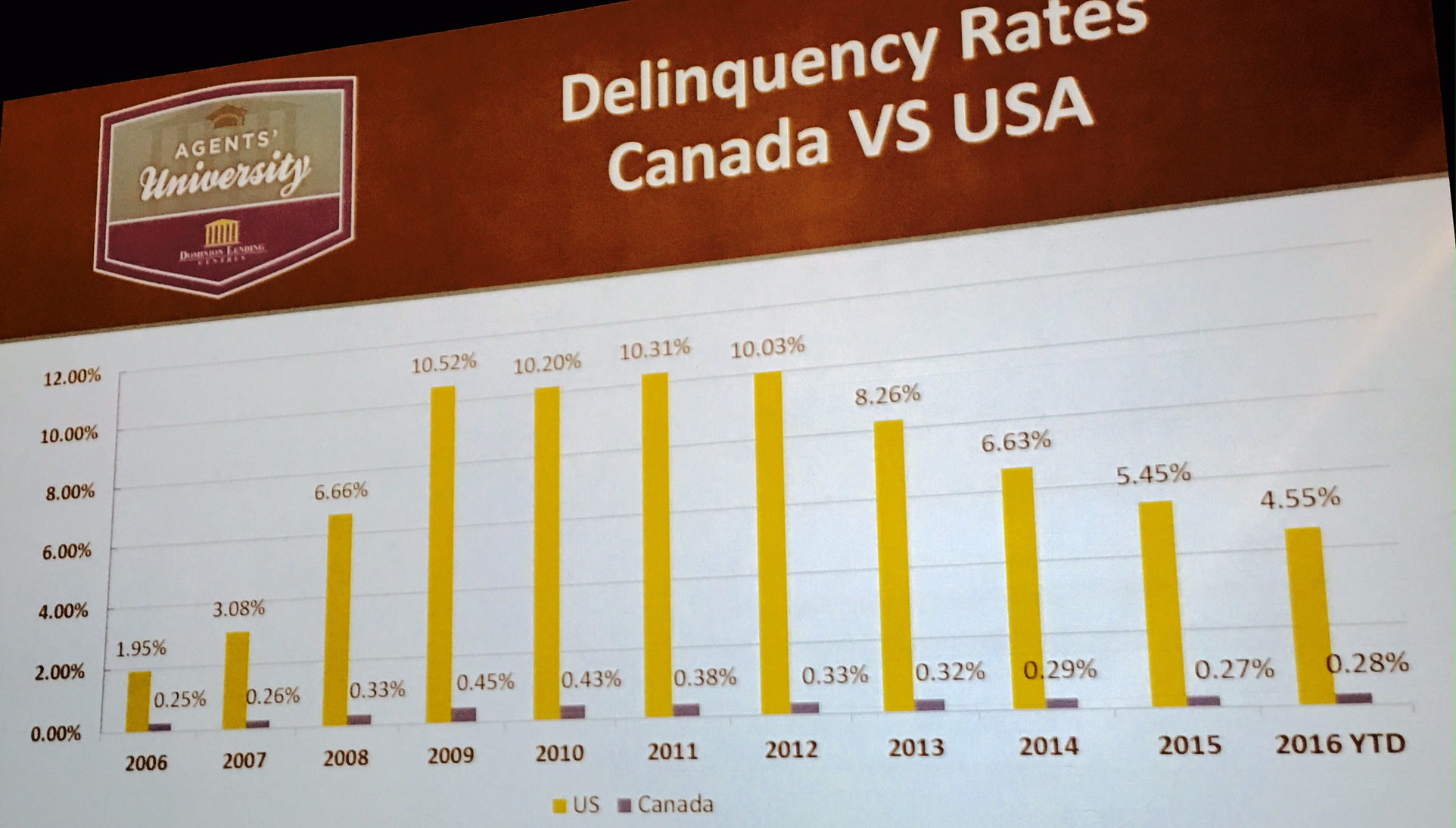

Well, they should get themselves a $20,000 raise before they buy what they could have bought. Exactly what so many before them have bought, and what just ~0.30% of CDN’s ever stop making payments on.

Wasn’t the 2008 financial crisis a ‘stress-test’ of CDN households? We came through that intact, far more so than our counterparts to the south.

What fire is the government trying to put out here?

The Provincial Government

Without question the BC provincial government threw a psychological bucket of cold water on the entire market with it’s poorly implemented foreign buyer tax. And lets be realistic, if they had truly wanted to limit foreign ownership they would have restricted foreign buyers to owning a single CDN property, or at the least a single BC property. instead they said ‘give us more money’ and keep on coming. If a 33% rise in one year did not slow down foreign buyers, what are we thinking a 15% tax will do once 6-12 months pass and it is normalized into the market?

Bottom line is that nobody knows what it will do, with so many transactions pulled from Aug, Sept, Oct into that final week of July to beat that tax, we once again do not have clean data. We will over the coming months, and until then many of us are are holding our collective breath and pressing pause to just ‘wait and see what happens’. But prices, especially in that bottom 80% of listings, are not really moving at all. Not yet.

The Municipal Government

Talk to a home-builder about the level of municipal red-tape, fees and taxation involved in their adding new supply to any market in the Greater Vancouver area.

Development fees, and costly red-tape delays (time is money) all conspire, with other levels of government to place an estimated $109,000.00 of a $400,000.00 condo into the hands of various levels of government.

25% of the cost of new housing is taxation.

A golden goose for government to say the least.

Conclusion

With any product, there will always be the top 20% of premium offerings that few among us are able to afford. Clothing, cars, watches, or handbags, there are always products out of our personal price range. We do not look at the average cost of a suit, a car, a handbag before we purchase it, we look at what we can afford. Purchasing a home is similar.

It is short-sighted to focus primarily on average prices as the media does. These numbers skew our perceptions because of the incredibly high-end properties in our markets. But hey, that $50,000,000.00 sale sells newspapers and generates clicks, so that is the one we have our attention guided to, but what we focus on is often not reflective of reality as a whole.

The average buyer has more options available than they realize, although the various levels of government are doing what they can to reduce those options.

When you hear terms like ‘suck some demand out of the market‘ – what they really mean is ‘suck buyers with lower household incomes out of the market‘. Maybe that is you, your siblings, your adult children? Were they really at risk? Do they really need the level of coddling we now have in place? Arguably no, because they already had great credit, zero debt, strong income, and a down payment.

How tightly do you want the government dictating your financial affairs?

Dustan Woodhouse[/vc_column][/vc_row]

Good analysis Dustan. The bottom 80% is a much more realistic snapshot of the market. Provincially this is the government buying votes for the next election. Federally, this is the government trying to stay relevant after a year in power. In both cases (particularly provincially), I don’t believe the government understood the impact their measures would have nor did they consult anybody who understands the real estate market. “Psychological bucket of cold water” is a good way to describe it. If the economy stays strong in Vancouver, the psychological effect will fade in a couple months luckily.